Texas 2-Step Renovation Loan

Financing for Remodeling and Repairs

The Texas 2-Step Renovation Program is the perfect solution for many individuals seeking to acquire a property needing significant repairs or remodeling.

Although Retiro Financial offers the FHA 203(k), Fannie Mae and Freddie Mac single-closing renovation loans for this type of transaction, our proprietary Texas-2-Step Renovation Program will typically result in superior financing terms and will often permit a buyer to avoid mortgage insurance without a 20% down-payment or cash-outlay.

That’s because the FHA, Fannie Mae, and Freddie Mac programs use the cost of acquisition and improvements to determine the maximum loan amount and loan-to-value ratio. The Retiro Financial Texas 2-Step will utilize the appraised value of the renovated property.

Let’s look at an example to illustrate this difference.

Let’s assume you’re a potential homebuyer seeking to purchase a primary residence in a neighborhood where remodeled homes sell at a premium. You found a property that needs significant remodeling. You can acquire this property for $400,000 in its current condition. It needs $100,000 of repairs and remodeling, including foundation work and partial roof replacement. In its current condition, the appraised value is $400,000. But with the contemplated remodeling it would appraise for $580,000. This is a common scenario.

With the agency renovation loans, the deemed value is the cost of acquisition plus the cost of improvements even if the property appraises for much higher than that amount. Thus, to avoid mortgage insurance, you’d be limited to a loan amount of $400,000 (80% of $500,000) and your total cash outlay would be $100,000. Yet with the Texas-2-Step the value is the value of the property after remodeling ($580,000) and you can borrow up to $464,000 (80% of $580,000) without the requirement of PMI, requiring a cash outlay of $36,000 plus closing costs, instead of $100,000, plus costs.

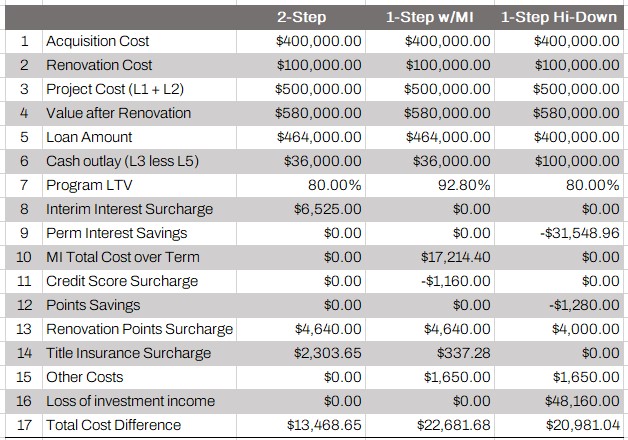

The following table illustrates the difference in cost associated with the various renovation programs when compared to a similar loan amount on a standard purchase or refinance. In reviewing the table keep in mind that the renovation options, although having higher transactions costs, result in an immediate $80,000 increase in property value, making it economically superior to the non-renovation alternative. This would only be the case when the post-renovation value exceeds the project cost as it does in our example. Many factors affect the advantage of one program over another. These include the ratio of renovation cost to acquisition cost (purchase price), the amount of cash outlay (affecting LTV ratio), and the borrower's credit score. Retiro Financial loan consultants determine the best option for the borrower based on the particular borrower and transaction characteristics and objectives.

The Texas-2-Step is also beneficial for investors seeking to purchase properties with a cash-outlay of less than the 20% to 25% that is typically required on conforming investor purchase transactions. An investor could utilize our example in the preceding paragraph to purchase the property, without PMI, with a cash-outlay (down-payment) of less of 7.2% of the transaction amount. This type of property, acquired below value, is ideal for an investor. Because it is acquired below value, during periods of low interest rates the property will typically cash-flow immediately, despite having nominal equity.

The Texas-2-Step is a fantastic program, designed to reduce the cash required to purchase a property with lower financing costs than on standard FHA, Fannie Mae and Freddie Mac programs that include financing of improvements. It’s best utilized on a transaction where the property will appraise for significantly more after contemplated improvements.

For properties where the cost of acquisition and renovation will not be substantially higher than the appraised value after renovation, an FHA 203(k) or the Fannie Mae HomeStyle or Freddie Mac Choice renovation programs may be a better choice. Learn more about those programs here.