The Closing Disclosure

The Closing Disclosure for Mortgage Loans Explained

Before finalizing your home loan, a critical document to thoroughly examine is the closing disclosure. Spanning five pages, it meticulously outlines the ultimate terms and expenses linked with your mortgage. This document serves as your final opportunity to confirm the accuracy of all figures prior to your closing.

Understanding the regulations and your entitlements pertaining to the closing disclosure empowers you to rectify any inaccuracies and affords you the necessary time to ascertain that the loan aligns with your best interests.

What is a closing disclosure?

The closing disclosure is a comprehensive five-page legal document that delineates the definitive terms of the mortgage loan you are poised to obtain. It furnishes essential details such as your interest rate, closing expenses, loan terms, monthly payment, and various other pertinent facets of your mortgage.

Dissimilar to the initial loan estimate provided at the onset of the loan proceedings, the closing disclosure presents a conclusive breakdown of the financial specifics for your scrutiny before you affix your signature to the final mortgage documentation during your closing. Once you have thoroughly examined and sanctioned your closing disclosure, you are primed to conclude the mortgage procedure, finalize your loan, and acquire possession of the keys to your new home or conclude your refinancing endeavor.

Why a closing disclosure is important

The closing disclosure provides a final chance to ensure your comfort with borrowing in accordance with the terms of the initially applied loan. Moreover, it serves as a mechanism to hold the lender responsible for the precision of its initial estimates and, in certain instances, mandates the lender to cover expenses that were inaccurately disclosed.

The closing disclosure mandates a compulsory three-business-day duration for scrutinizing all figures to ensure proper crediting for prepaid items, such as appraisal fees or earnest money deposits. Additionally, it verifies the application of any seller or lender credits towards the closing amount owed.

About the closing disclosure 3-day rule

To ensure sufficient opportunity for reviewing all financial details prior to finalizing paperwork, lenders are legally mandated to furnish a closing disclosure at least three business days prior to the scheduled closing date. Instituted by the Consumer Financial Protection Bureau (CFPB) in 2015, this waiting period aims to prevent homebuyers from feeling pressured into accepting loans beyond their financial means, based on terms revealed only at the closing table.

During this period, homebuyers can meticulously examine the documentation with their loan officer, and if necessary, seek guidance from legal counsel or regulatory authorities if discrepancies arise from the initially applied terms. Allocating additional time for this obligatory waiting period is crucial for ensuring timely closure when purchasing a home.

The Closing Disclosure – A page-by-page look

The main objective of the closing disclosure is to cross-reference it with your initial loan estimate to ensure consistency of information. Ideally, there should be minimal deviations, with figures closely aligning with your loan estimate, barring minor adjustments for factors like interest, property taxes, homeowner’s insurance, and prepaid interest prorations. For a comprehensive understanding of each page, the Consumer Financial Protection Bureau (CFPB) offers a comprehensive guide to dissecting the closing disclosure.

We've outlined key points to consider on each page as you conclude your mortgage process.

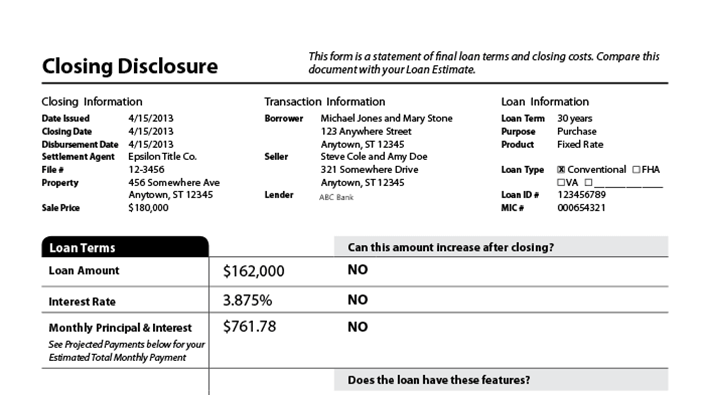

Page 1

The initial page of your closing disclosure presents a summary of key aspects of your mortgage, encompassing:

- Loan information: This segment should mirror the details outlined in your loan estimate regarding the loan term, purpose, and program type (e.g., conventional, FHA, VA, or USDA).

- Loan terms: Exercise caution while reviewing this section as it outlines information concerning your final loan amount, interest rate, and monthly payment, focusing solely on the principal and interest calculation.

- Projected payments: Here, you'll find an overview of your total final principal, interest, taxes, and insurance (PITI) payment at the closing moment and throughout the loan's lifespan. The "estimated escrow" amount encompasses property taxes and homeowners insurance if you opt to include them in your payment. Additionally, the projected payment may encompass mortgage insurance if your down payment is less than 20% on a conventional loan or if you're obtaining a Federal Housing Administration (FHA) loan. Private mortgage insurance (PMI) is the most common type, safeguarding conventional lenders from losses in case of payment default. For FHA loans, you'll encounter two types of mortgage insurance: an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP) integrated into your monthly payment.

- Costs at closing: This section delineates your "cash to close," providing a fundamental breakdown of any expenses covered by the seller or lender on your behalf. You'll be required to issue a cashier's check or wire the designated amount to settle any outstanding closing costs and the down payment owed on the loan. If discrepancies arise, review the itemizations of all credits and charges on Page 2.

Page 2

This page resembles the former HUD-1 settlement statement, which borrowers used to scrutinize mortgage figures prior to 2015, and offers a detailed breakdown of all transaction costs. Sections A, B, and C delineate loan costs, regulated by federal law.

Fees that are immutable after the signing of a closing disclosure should match those initially outlined in your loan estimate. Any disparities should result in a reimbursement from your lender. These unalterable fees encompass:

- Origination charges

- Mortgage points

- Appraisal costs

- Credit report fees

- Flood monitoring expenses

- Flood determination charges

- Tax monitoring costs

- Tax status research fees

- Transfer taxes

Remaining costs fall into two categories: those subject to a maximum 10% increase and those with no specified limit.

Fees limited to a 10% increase comprise:

- Recording charges

- Pest inspection fees

- Survey costs

- Title insurance premiums

- Title settlement agent fees

- Title search expenses

Conversely, the following fees have no predefined limit on potential increases from the initial quote:

- Homeowners insurance premiums

- Property taxes

- Prepaid interest

- Homeowners association (HOA) fees

- Home warranties

Page 3

Page 2 of the Closing Disclosure provides a summary of all of the itemizations ono Page 2. It outlines any credits you’ll receive from the seller or real estate agent on a purchase transaction and any credits from the mortgage lender. This is shown in section L under the “Paid already by or on behalf of borrower at closing” heading.

Page 4

On page 4 of the Closing Disclosure a few of the finer details of the mortgage loan are set out.

This page explains when your payment is considered late and the fee you’ll pay if it is. It also sets out whether your homeowner’s insurance and property taxes are included in your payment. The escrow section breaks down how much will be collected at closing and monthly to keep enough funds in your escrow account to pay your property-related bills when they come due.

Page 5

The annual percentage rate (APR) is shown on this page. APR is a federally mandated method of comparing loans with varying terms that attempts to express how the upfront costs paid on the mortgage loan would compare to a loan with no upfront costs. Check out our detailed explanation of APR in this article.

Page 5 also provides some other disclosures that explain what happens if you default on your payments and face foreclosure, and a list of everyone involved in the transaction in case you have questions after your closing.

Conclusion

The Closing Disclosure provides a detailed breakdown of all the costs association with your transaction and mortgage loan. It’s your last look at how the transaction will add up prior to going to the closing.